probably around 3k/month at leastWork benefit. It's a BCBS platinum plan that the company pays about 75% of the total cost.

Yeah I don't know how it works or what it costs on the open market.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

How the hell are we supposed to retire?

- Thread starter Red Mosquito

- Start date

mfennell

Well-Known Member

But I will be active and busy, and the image of a retiree turning into mush on the couch and being bored literally to death will be the furthest thing from my reality.

This right here. I have heard that there are people who have no real interests or even friends outside work. I can imagine that kind of person going south in a hurry. I don't know any of them though. It must get harder as your mobility winds down. I'm seeing it in my 78yo father, who broke his leg on his morning walk, then needed a knee replacement. He admits to taking forever to work up to performing fairly trivial tasks around the house.

Hey, if you're able to live frugally and make that happen, God Bless Ya!I do not spend $150k a year lol good God. Nor do we make $300k a year unfortunately.

Your calculation isn't accounting for taxes. In that scenario the person making $300k and saving $150k a year is living on $70k a year. 4 million withdrawn at a 3% rate is $120k annually so that's a huge window.

And again... Based on the Trinity study that's basically guaranteed to last your entire retirement.

I think most people start spending more when they are making more, I know I did. You go out to eat more often, everything the kids do cost a pretty penny.

Shit, just to get me and my family to vacation is usually 2k, sometimes more. Rarely, it less. That's just the flight! There are 4 of us. Then as your kids get older, wow does the money fly. Just think, its 4 times as much to do anything! But the joy they bring is worth every penny, the ajita, not so much!

everything the kids do cost a pretty penny.

That's the key lol, none of those. Getting snipped later this year actually.

No doubt, that will make a big difference. And if you don't want them, don't have them. Really though, there is no more joy than when you kid does something to make you proud, even when you know, you had absolutely nothing to do with it.That's the key lol, none of those. Getting snipped later this year actually.

No doubt, that will make a big difference. And if you don't want them, don't have them. Really though, there is no more joy than when you kid does something to make you proud, even when you know, you had absolutely nothing to do with it.

Yep, different folks for different strokes. I got way more in the con column to having kids. Having 2 nieces and 2 nephews helps satiate the need for sure. More power to people who want them...not for me.

Yep, different folks for different strokes. I got way more in the con column to having kids. Having 2 nieces and 2 nephews helps justifying getting snipped. More power to people who want them...not for me.

Yeah man, if you don't want to have kids, DON'T!!Yep, different folks for different strokes. I got way more in the con column to having kids. Having 2 nieces and 2 nephews helps satiate the need for sure. More power to people who want them...not for me.

I know a lot of people who probably shouldn't have had any.

thegock

Well-Known Member

Sorry Rick you provided nothing worthwhile into the discussion.

You jumped in with a ny times article and have followed it up with emojis and personal opinions.

At least he didn't post a picture of the sexual predator Vince McHand

Fire Lord Jim

Well-Known Member

I know a lot of people whose parents shouldn't have had any!I know a lot of people who probably shouldn't have had any.

Fire Lord Jim

Well-Known Member

The following is for after-tax accounts. If everything is §401K or IRA, move along, nothing to see.

Some readers may know that I am not a fan of index funds. Here's where holding index funds can give you an unwelcomed tax surprise this year. This applies to more than index funds, and to any fund with a low turn-over rate. For this example I will use the S&P 500 funds.

American Express was added to the S&P 500 in 1976. I don't have data that far back, but in 1983 it was trading at $6. Today it trades at $146. But it was at at $195 in February. The market had a "correction" and the S&P 500 is down 20% year to date. You are a buy and hold investor, you didn't get scared and sell. But plenty others did. And, it turns out, you sort of did sell. How's that?

Each stock in the S&P 500 has a weight and a ranking. When hordes of scared investors sold, the fund managers had to sell stocks to cash out the selling fund holders. And with that weighting, they can't just sell the losers, but they sell a bit of everything to maintain the weight and ranking. Someone you don't know sold his S&P 500 holdings, the fund manager sold stocks to meet that cash-out transaction, and American Express got sold at a huge capital gain. Even though it dropped from its February high of $195 to $146, the cost basis to the fund was $6, and what looks like a loss to us is a gain in the fund. These funds maintain their tax exempt status by distributing the capital gains and dividends to the fund holders each year. So we can expect a huge capital gain distribution in the year when we are down 20%! A taxable gain without the gain. This is a feature of the inside basis of the stocks in the fund, vs the outside basis to us—the cost we paid for the funds. If we held stocks instead of funds, other people selling would not generate capital gains to us. We can still decide when to get income.

The surprise taxable gain can cause big headaches, as it can throw your income over limits you may have been planning to stay under:

Some readers may know that I am not a fan of index funds. Here's where holding index funds can give you an unwelcomed tax surprise this year. This applies to more than index funds, and to any fund with a low turn-over rate. For this example I will use the S&P 500 funds.

American Express was added to the S&P 500 in 1976. I don't have data that far back, but in 1983 it was trading at $6. Today it trades at $146. But it was at at $195 in February. The market had a "correction" and the S&P 500 is down 20% year to date. You are a buy and hold investor, you didn't get scared and sell. But plenty others did. And, it turns out, you sort of did sell. How's that?

Each stock in the S&P 500 has a weight and a ranking. When hordes of scared investors sold, the fund managers had to sell stocks to cash out the selling fund holders. And with that weighting, they can't just sell the losers, but they sell a bit of everything to maintain the weight and ranking. Someone you don't know sold his S&P 500 holdings, the fund manager sold stocks to meet that cash-out transaction, and American Express got sold at a huge capital gain. Even though it dropped from its February high of $195 to $146, the cost basis to the fund was $6, and what looks like a loss to us is a gain in the fund. These funds maintain their tax exempt status by distributing the capital gains and dividends to the fund holders each year. So we can expect a huge capital gain distribution in the year when we are down 20%! A taxable gain without the gain. This is a feature of the inside basis of the stocks in the fund, vs the outside basis to us—the cost we paid for the funds. If we held stocks instead of funds, other people selling would not generate capital gains to us. We can still decide when to get income.

The surprise taxable gain can cause big headaches, as it can throw your income over limits you may have been planning to stay under:

- NJ retirement exclusion

- Medicare IRMAA levels

- Tax bracket planning

- FAFSA reporting

- Social Security taxation

- likely more that I can't think of right now

rick81721

Lothar

Zuckerberg is down $100 billion over the last 13 months. Still has about 40 billion left!

https://www.forbes.com/sites/jonath...rapples-with-recession-fears/?sh=5ae6aa7c176c

https://www.forbes.com/sites/jonath...rapples-with-recession-fears/?sh=5ae6aa7c176c

rick81721

Lothar

Social Security - take it early, at retirement age or delay until 70? There are advocates for all three options here. If you are depending on it as a major portion of retirement income, and you think (hope) you will live a long time, probably better to wait. But like most things in life, it's a gamble. Maybe you will live long enough to collect that higher amount for enough years to break even. Maybe you won't. Just an anecdotal n=2 story but I am going out to Chicago tomorrow for my best friend's wife's funeral. She was 62. Both retired a few years ago. My friend (just turned 62) was just diagnosed with glioblastoma a month ago. He will be lucky to live a few more months. Both worked 30+ years, paying into social security. Both won't see one dime in return.

I'm glad we started collecting early.

https://www.fool.com/investing/2022/08/13/should-you-wait-until-70-to-claim-social-security/

I'm glad we started collecting early.

https://www.fool.com/investing/2022/08/13/should-you-wait-until-70-to-claim-social-security/

thegock

Well-Known Member

Social Security - take it early, at retirement age or delay until 70? There are advocates for all three options here. If you are depending on it as a major portion of retirement income, and you think (hope) you will live a long time, probably better to wait. But like most things in life, it's a gamble. Maybe you will live long enough to collect that higher amount for enough years to break even. Maybe you won't. Just an anecdotal n=2 story but I am going out to Chicago tomorrow for my best friend's wife's funeral. She was 62. Both retired a few years ago. My friend (just turned 62) was just diagnosed with glioblastoma a month ago. He will be lucky to live a few more months. Both worked 30+ years, paying into social security. Both won't see one dime in return.

I'm glad we started collecting early.

https://www.fool.com/investing/2022/08/13/should-you-wait-until-70-to-claim-social-security/

Rick, u ignorant slut...

Now, the counterpoint for delaying SS benefits will be presented by @Fire Lord Jim :

Jumping on my company's HSA for next year so I'll be putting in ~30k into retirement in 2023, my highest ever.

www.madfientist.com

www.madfientist.com

Pretty excited to have access to that account for the first time.

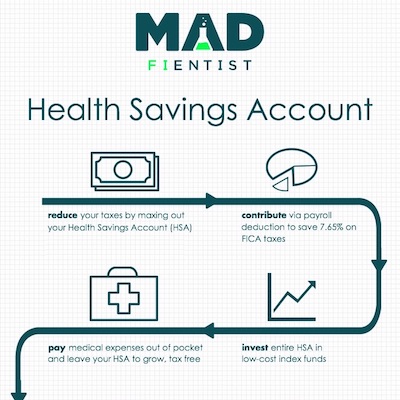

HSA - The Ultimate Retirement Account

A Health Savings Account (HSA) is the ultimate retirement account because it can provide completely tax-free savings for early retirement!

Pretty excited to have access to that account for the first time.

rick81721

Lothar

Rick, u ignorant slut...

Now, the counterpoint for delaying SS benefits will be presented by @Fire Lord Jim :

View attachment 202194

The counterpoint is obvious. But it's a gamble. You might end up getting more, you might end up getting less, you might get bupkis. I'd rather get something now when I can enjoy it vs potentially more when I don't need it and possibly not be able to enjoy it. Ymmv!

rick81721

Lothar

Jumping on my company's HSA for next year so I'll be putting in ~30k into retirement in 2023, my highest ever.

HSA - The Ultimate Retirement Account

A Health Savings Account (HSA) is the ultimate retirement account because it can provide completely tax-free savings for early retirement!

Pretty excited to have access to that account for the first time.

Did they change the rules on those? When I was working, you had to use the money by the end of the year (I think).

Did they change the rules on those? When I was working, you had to use the money by the end of the year (I think).

That would be an FSA which does have to be used (some companies allow a small $500ish annual rollover). Still pre tax and nice to have but not nearly as advantageous for retirement.

rick81721

Lothar

That would be an FSA which does have to be used (some companies allow a small $500ish annual rollover). Still pre tax and nice to have but not nearly as advantageous for retirement.

Interesting. I guess we were never offered the option as we didn't have high deductible health insurance plans.

Fire Lord Jim

Well-Known Member

I bolded Rick's text above.Social Security - take it early, at retirement age or delay until 70? There are advocates for all three options here. If you are depending on it as a major portion of retirement income, and you think (hope) you will live a long time, probably better to wait. But like most things in life, it's a gamble. Maybe you will live long enough to collect that higher amount for enough years to break even. Maybe you won't. Just an anecdotal n=2 story but I am going out to Chicago tomorrow for my best friend's wife's funeral. She was 62. Both retired a few years ago. My friend (just turned 62) was just diagnosed with glioblastoma a month ago. He will be lucky to live a few more months. Both worked 30+ years, paying into social security. Both won't see one dime in return.

I'm glad we started collecting early.

https://www.fool.com/investing/2022/08/13/should-you-wait-until-70-to-claim-social-security/

Break-even is the wrong tool for valuing insurance. Do you have fire insurance? A fire extinguisher? What is your break-even on buying those? When buying insurance, put the break-even tools away. The proper measure for insurance is how much loss can you absorb. Like choosing a deductible. Then pay for whatever coverage you can't absorb. Running out of money when we are too old to work is a loss we can't absorb.

View Social Security as a tax until age 62, then an annuity after that. The question isn't whether I get more money by claiming early or later, but rather are we insuring against running out of money when we are old? Claiming at age 70 pays nearly twice a month what an age 62 claimant gets. Do you really want to be hitting your 60 year old kids up for money to pay your bills? You think you have enough money already? Have you priced assisted living and nursing homes? Do you think that the 9% inflation we just saw will make medical and nursing home prices go down?

I could die before I ever collect. Guess what? In that case, I didn't need the money. But I could live... a long time. Social Security is designed to give the same amount over the average lifetime no matter when we start to collect. If your break-even analysis says different, you used the wrong discount rate, or the wrong number of payments. Now for the fun part. We ride bikes. We live in the Northeast, some of the wealthiest areas of the US. We are not average. Social Security's average lifetime averages male and female, black and white, urban and suburban, rich and poor diabetic and mountain biker. It does not differentiate even though females outlive males, wealthy outlive the poor, healthy and active outlive the couch potatoes. Plus medical intervention continues to get better. We are very likely to be collecting Social Security for a very long time. I will claim at age 70 unless my doctor finds a reason not to.